Debt is often seen in black and white terms: you either have it, or you don’t. But the reality is much more nuanced. Just as income has different brackets, so does debt. The levels of debt you experience can drastically influence your lifestyle, choices, and ultimately your freedom.

Depending on where you stand in this system, debt can either be a trap, a tool for growth, or a stepping stone to building something unassailable. Let’s explore the ten levels of debt and how each one can shape your life.

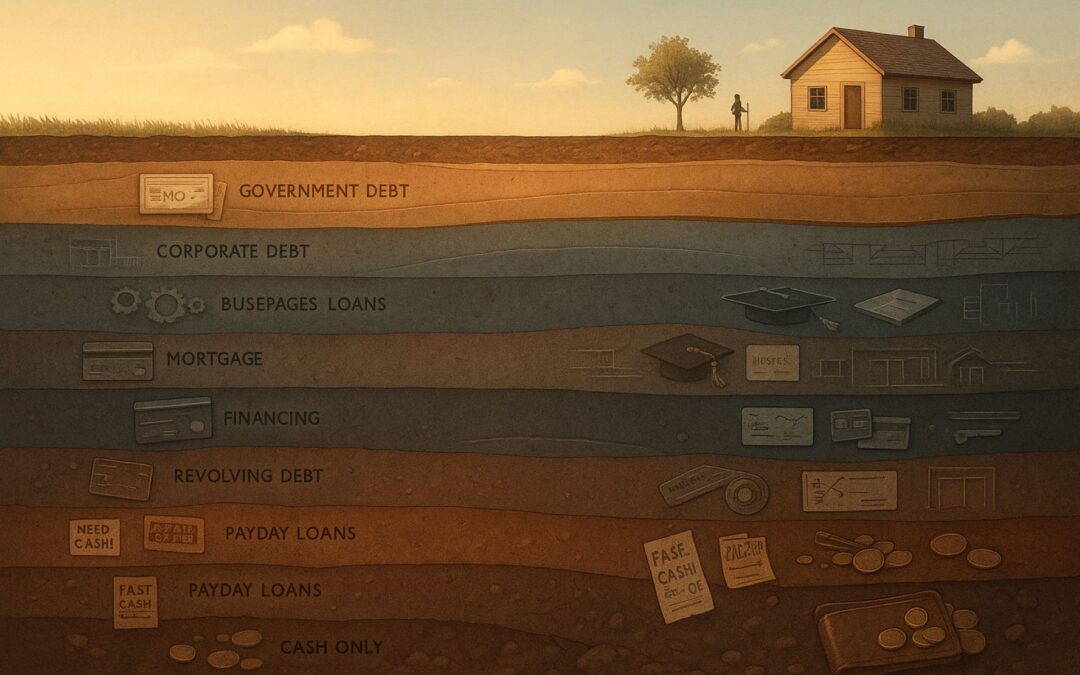

Level 1: Cash Only

At Level 1, debt doesn’t exist, and financial independence takes on its most basic and unadulterated form: living purely on cash. This level is often regarded as the ideal, where you owe no one anything, have no credit cards, loans, or financial obligations hanging over your head. It’s a state where your spending is restricted to what you have in your pocket or your bank account. In one sense, this lifestyle offers the purest form of financial freedom, as you aren’t tethered to any institutions or creditors. There’s no worrying about missed payments, mounting interest, or the obligations that come with borrowing money.

However, this type of financial independence is accompanied by significant limitations. The first category of people who might find themselves living this way are those who practice extreme frugality. They live far below their means, often choosing not to indulge in luxuries or material possessions. For these individuals, financial freedom is not measured by assets or credit but by their ability to save and control spending. They may not own much—no car, no house, and very few material possessions—but they live a minimalist lifestyle, prioritizing savings and avoiding unnecessary debt. These people may not be in debt, but they also may not have the ability to invest or grow wealth through traditional means.

On the other end of the spectrum, those who are homeless, unhoused, or struggling without a permanent place to live also technically exist at this level, as they too owe no one anything. However, it’s important to note that this lack of debt does not equate to financial stability. In fact, those living without a home may not be financially independent at all, as they lack the resources to control their lives in meaningful ways. While they owe no money, they are often more financially vulnerable than people carrying debts but with a steady income.

The cash-only lifestyle is a double-edged sword. It provides a sense of safety in that you don’t risk owing anyone anything, but it also traps you in a financial situation where growth is difficult. Without access to credit or borrowing power, you can’t build your credit score, buy property through loans, or leverage financial tools to grow wealth. You can’t scale your life or business because there’s no financial flexibility. This lifestyle can keep you financially small and static—safe from the perils of debt, but stuck in a state of financial inertia.

The real dilemma at this level is deciding whether living debt-free is actually holding you back or protecting you from greater risks. Are you maintaining this lifestyle to safeguard yourself from future debt, or are you choosing a path that keeps you small because you fear the potential consequences of borrowing? Cash-only living doesn’t pose immediate survival challenges, but it requires a conscious decision about whether you’re simply staying stagnant or consciously choosing to stay in a place of minimal risk.

Level 2: Payday Loans

Level 2 introduces a shift into the realm of borrowing, but it’s a dangerous type of borrowing—payday loans. This form of debt often begins when you find yourself in a financial pinch, such as needing money to pay rent, repair your car, or cover some emergency expense, all while knowing that your next paycheck is still days away. Payday loans represent an easy, immediate fix, offering quick access to cash without much paperwork or credit checks. But these loans often come at a steep price, and that price is not just financial, but also psychological and emotional.

The structure of payday loans is deceptively simple. You borrow a small amount of money, usually between $100 and $1,000, and repay it with your next paycheck. What seems like a short-term solution to a temporary problem often spirals into a long-term struggle due to the extremely high interest rates attached to these loans. The cost of borrowing becomes astronomical once you factor in the interest, which can range anywhere from 200% to 600%, depending on the state and the lender.

The problem with payday loans is that they are designed to trap you. Since payday loans have short repayment periods, the interest rate accrues quickly. If you can’t repay the full loan on time, you’ll end up taking out a new payday loan just to cover the old one, with more interest piled on top of the original amount. This creates a debt cycle that is incredibly hard to break. Many people who use payday loans are not reckless or irresponsible, but instead, they are often working full-time jobs, earning modest incomes (often under $40,000 a year), and living paycheck to paycheck. They don’t have savings or an emergency fund, so they turn to payday loans to make it through tough weeks.

In fact, payday loans are not used exclusively by those living in poverty or those making reckless financial choices. Millions of hardworking individuals use payday loans regularly as a temporary solution to cover gaps in their financial situation. However, this borrowing is not a temporary fix. It becomes a continuous cycle for many, as they end up taking out an average of eight payday loans per year, often paying exorbitant fees and interest rates. Payday loans are not inherently evil or exploitative in nature, but they often become predatory for people who struggle financially and are looking for immediate relief.

The biggest problem with payday loans is the psychological impact they have on borrowers. When you borrow money like this, you don’t just face financial consequences—you face emotional strain. The stress of knowing you have an outstanding loan and the pressure of meeting the payment deadlines can wreak havoc on mental well-being. For people already struggling with financial insecurity, the last thing they need is to fall deeper into debt due to desperation.

Payday loans seem like a quick way to get money now, but the long-term consequences are far more damaging. The reliance on payday loans reinforces a cycle of debt, where people are always borrowing just to make ends meet. Breaking free from this cycle requires more than just financial discipline—it demands creating an emergency fund, building a stable income, and ultimately finding ways to avoid relying on high-interest, short-term loans. Until then, payday loans remain a trap that prevents financial growth and keeps individuals locked in a cycle of debt.

Level 3: Revolving Debt (Credit Cards)

Revolving debt, primarily through credit cards, represents one of the most insidious levels of borrowing because it is so easy to fall into and difficult to escape. Credit cards are marketed as a tool for financial flexibility and convenience, offering you the ability to make purchases now and pay for them later. The draw is simple: you get what you want today, and the payment can be deferred until the end of the billing cycle. However, once you fail to pay off the balance in full, you begin to enter the dangerous territory of accruing interest, which makes revolving debt a persistent and potentially crippling financial trap.

The way credit cards work is that you are given a credit limit, and when you make purchases, the card issuer covers the cost. If you pay the full balance by the due date, you avoid any interest charges, and there’s no additional cost to you. However, if you are unable to pay off the full balance, the credit card issuer starts charging interest on the outstanding amount. Interest rates on credit cards can range from 15% to 30% annually, depending on the issuer, your creditworthiness, and your payment history.

What makes credit card debt so dangerous is the way interest compounds. If you make only the minimum payment (usually just a small percentage of your balance), it may feel like you’re making progress, but in reality, you’re barely making a dent in the principal amount you owe. The interest charges continue to pile up month after month, and because your payments are going primarily toward covering the interest, the balance hardly decreases. Over time, this can result in a situation where you owe far more than you initially spent.

The average American carries around $6,000 to $8,000 in credit card debt by their 30s. This is a staggering amount when considering that many individuals begin to use credit cards at an early age and continue to rely on them throughout their lives. In fact, for many, credit cards are often the first form of debt they encounter. While credit cards can provide a valuable tool for building a credit score and offering purchase protection, the reality is that they often lead to the accumulation of debt that can be difficult to escape.

The history of credit card usage in America reveals just how widespread and ingrained this type of debt has become. Back in the 1950s, banks were eager to expand their credit card base, and as a result, they began sending unsolicited credit cards to millions of people without requiring any background checks. This marketing strategy, which seemed like an easy way for banks to grow their customer base, quickly normalized the idea of revolving debt. Today, it’s not unusual to receive credit card offers in the mail, and credit card debt has become a cultural norm.

One of the most concerning aspects of credit card debt is the psychological trap it creates. The allure of buying something now and paying for it later can be irresistible, especially when you’re living paycheck to paycheck or just starting out financially. The immediate satisfaction of purchasing a desired item can outweigh the long-term consequences of carrying a balance. Over time, this cycle of debt becomes habitual. Once you carry a balance on your credit card, it can become harder and harder to pay it off, especially as you continue to accumulate new charges and interest fees.

For those looking to escape the revolving debt cycle, the most important first step is to take a hard look at spending habits. High-interest debt can be debilitating, and when credit cards are involved, the cycle can feel impossible to break. Paying off credit card debt requires discipline, budgeting, and often a sacrifice of lifestyle in the short term to achieve long-term financial freedom. It is essential to avoid adding to the debt by cutting unnecessary expenses, paying more than the minimum payment, and paying off the highest-interest debts first. Until the balance is paid in full, credit card debt will continue to serve as a financial ball and chain, restricting your ability to invest, save, or build wealth.

Level 4: Financing

Financing takes credit card debt to a new level, introducing higher-dollar, longer-term commitments that lock you into more significant financial obligations. At this stage, you’re not just borrowing for a small purchase; you’re borrowing to fund larger, long-term purchases like cars, furniture, or even high-end electronics. Financing differs from revolving credit in that it usually involves fixed monthly payments over a longer period, typically ranging from a few months to several years.

The concept of financing appeals to people because it allows for immediate gratification—whether it’s the purchase of a car, new furniture for your home, or the latest technology—but the cost is much higher than it initially appears. Unlike credit cards, where interest is calculated monthly, financing deals often extend over multiple years, during which time the item you’re buying will lose value. Take the example of a car: the moment you drive it off the lot, it begins to depreciate in value, yet you’re still obligated to make monthly payments for years to come. In the end, you’ve paid full price for an asset that is no longer worth what you initially paid for it.

When you finance an item, the lender typically covers the cost of the purchase upfront, and you agree to repay them in monthly installments with interest over time. It can seem like a good deal because the payments are broken down into manageable amounts, but these manageable amounts often don’t take into account the total cost of the purchase. Over the term of a loan, you could end up paying much more than the original price of the item because of interest charges and fees. For example, a $30,000 car financed over five years with a 7% interest rate might cost you more than $35,000 by the time the loan is paid off.

What makes financing especially dangerous is that it becomes a way to live beyond your means. You can acquire more expensive items than you would normally be able to afford, but the long-term impact of that borrowing is a constant monthly burden. Many people get into financing without considering the full implications—how long they’ll be paying it off, whether they’ll still want or need the item in a few years, and what other opportunities they could pursue with that monthly payment.

Financing also tends to be marketed in a way that makes it feel like a savvy financial decision. For example, retailers often offer “no interest for 12 months” deals or “low monthly payments,” which sound tempting but fail to highlight the hidden costs. If you miss a payment or fail to repay the loan in the agreed-upon time, the interest can accumulate at an alarming rate, turning a seemingly affordable purchase into a major financial burden.

At this level of debt, the line between necessity and luxury blurs. The temptation to finance items like cars or home improvements is strong, but the reality is that you’re often borrowing for depreciating assets that lose value over time. This is why it’s crucial to evaluate the purpose of the borrowing. Are you financing something that will help you grow financially or something that will only further entrench you in debt? If you’re financing for a practical investment, like starting a business or purchasing a home that will increase in value, it might be a worthwhile investment. However, if you’re financing consumer goods that lose value, you’re only digging yourself into a deeper financial hole.

The most important thing when it comes to financing is to borrow responsibly. You must understand the long-term commitment involved and assess whether the item you’re financing will truly add value to your life or your financial situation. If you’re taking on financing, it should be for something that appreciates in value or can help you create wealth in the future—like an education, a property, or an investment in your business. Everything else should be carefully scrutinized, as it may lead to years of financial strain and regret.

Level 5: Student Loans

Student loans represent a significant milestone in the journey through debt. At this level, debt takes on a different flavor—one that is often framed as “good debt” because it’s tied to education and the promise of future earnings. The idea behind student loans is that you borrow money to invest in your future. With a degree or advanced training, you’re expected to secure a better-paying job, which, in turn, will make repaying the loan more manageable. The reasoning behind this is simple: education is an investment in your future earning potential.

However, the reality of student loans often diverges significantly from this optimistic narrative. In the United States alone, over 44 million people owe a total of more than $1.7 trillion in student loan debt, making it one of the most significant sources of debt in the country. The average student loan borrower graduates with a debt load that can range from tens of thousands to over $100,000, depending on the school they attend, the degree they pursue, and whether they rely on federal or private loans.

The problem arises when students graduate and enter the workforce. While having a degree can certainly open doors, it doesn’t automatically guarantee a well-paying job, and the reality of the job market often falls short of expectations. Many graduates find themselves struggling to land a high-paying job, and as they face entry-level salaries, their student loan payments begin to feel burdensome. This is compounded by the fact that student loan repayment often starts immediately after graduation, putting further financial strain on individuals who may not have secured stable employment yet.

Even for those who do find a job, the sheer amount of debt can delay or prevent major life milestones, such as buying a home, starting a family, or even saving for retirement. The average student loan repayment period is about 20 years, meaning that many borrowers will still be paying off their loans well into their 40s or 50s, long after they’ve graduated. And while some may argue that a degree is an investment in long-term earning potential, many graduates find themselves living paycheck to paycheck as they struggle with their student loan payments.

Student loans also carry a psychological burden. The weight of student loan debt can affect your mental and emotional well-being, especially when paired with financial insecurity. As borrowers continue to make payments on loans that often feel unmanageable, they experience stress and anxiety, which can impair their decision-making and overall quality of life.

The challenge with student loans is that, despite their classification as “good debt,” they do not always provide a clear path to financial success. Many borrowers struggle with high-interest rates, complex repayment terms, and long payoff periods, which makes student loans one of the most challenging forms of debt to manage. In some cases, students may even default on their loans, which can have long-term consequences, such as damaged credit scores, wage garnishments, and difficulty securing future loans.

The most important consideration when it comes to student loans is not just borrowing the money, but understanding how it will affect your long-term financial situation. While education can be an invaluable asset, it’s essential to weigh the cost of borrowing against the potential return on investment. Will the degree lead to a higher-paying job, or will it simply create a large debt burden with little payoff? If you do take out student loans, it’s critical to be strategic about the programs you pursue and the schools you attend, ensuring that your education provides value that exceeds the cost of borrowing.

Level 6: Mortgage

A mortgage is typically the largest loan a person will take out in their lifetime, and it’s often seen as the gateway to homeownership. At this level, debt moves beyond consumer purchases and into real estate, a long-term investment that many view as a necessary part of building wealth. Mortgages are commonly framed as “good debt” because they are used to purchase a tangible asset—property—which is expected to appreciate in value over time. Homeownership is often associated with financial stability and success, and for many people, owning a home is a key part of the American Dream.

However, while the idea of owning a home is enticing, a mortgage comes with a significant amount of risk and responsibility. When you take out a mortgage, you are essentially agreeing to pay back the loan over the course of 20 to 30 years, often with a fixed interest rate. The bank or lending institution provides you with the funds to purchase the home, but in exchange, they retain a claim over the property until the loan is paid off. The property serves as collateral, and if you fail to make payments, the bank can foreclose on your home and sell it to recover the debt.

One of the most significant risks associated with mortgages is the potential for market instability. The housing market is notoriously cyclical, with periods of rapid growth followed by sharp declines. The 2008 financial crisis serves as a stark reminder of how quickly mortgage debt can turn toxic when the market crashes. During the housing bubble, many people were approved for mortgages they couldn’t afford, and when the market collapsed, millions of homeowners were left with homes worth less than what they owed. This led to widespread foreclosures and financial devastation.

While mortgages are still considered “good debt” by many, they come with the responsibility of ensuring that you can afford the loan long term. You must have a stable income and a solid emergency fund to weather any financial setbacks. It’s important to remember that a mortgage is a long-term commitment that can last for decades, and during that time, your financial circumstances can change. If you lose your job, face a medical emergency, or experience other financial difficulties, it can become challenging to make the monthly payments. This is why it’s crucial to only take on a mortgage that aligns with your financial situation.

Another aspect of mortgages that people often overlook is the total cost of homeownership. While paying a mortgage builds equity in the property, it also comes with additional costs that aren’t immediately obvious. These include property taxes, home insurance, maintenance and repairs, and utilities. The cost of homeownership can quickly add up, and if your income doesn’t keep pace with these expenses, it can create significant financial stress.

One of the key factors in making a mortgage work for you is understanding your ability to repay it without stretching your finances too thin. The goal should be to buy a property that you can comfortably afford, taking into account all the hidden costs of homeownership. While buying a house can be a great investment in the long run, it’s important to keep in mind that the value of a home can fluctuate. A mortgage can also prevent you from taking financial risks, changing jobs, or pursuing other opportunities because of the long-term financial commitment involved.

A mortgage isn’t just a debt—it’s a financial strategy that, if managed correctly, can lead to wealth accumulation through home equity. However, if you stretch yourself too thin and buy more house than you can afford, it can quickly turn into a financial burden. Ultimately, the key to making a mortgage work for you is ensuring that your purchase aligns with your financial goals and that you have the resources to make the payments over time, without sacrificing your financial flexibility. A mortgage may seem like a necessary step toward building wealth, but it’s essential to weigh the costs and risks before committing to such a large, long-term obligation.

Level 7: Business Loans

At Level 7, debt transitions from being a personal financial burden to a strategic tool for business growth. Business loans are fundamentally different from personal loans in that they are not based on your individual creditworthiness or financial history, but rather on the potential success of your business. Borrowing at this level involves raising capital to scale your business, invest in new opportunities, or smooth out cash flow issues. Unlike personal debt, which is often seen as a necessary evil, business debt is a calculated risk. When used wisely, it can provide the funds needed to accelerate growth, increase revenue, and drive innovation.

Business loans come in various forms, including lines of credit, equipment financing, bridge loans, and term loans. A line of credit gives you access to a set amount of money that you can borrow as needed, which helps manage ongoing cash flow fluctuations. Equipment financing allows businesses to purchase machinery or technology and pay it off over time, while bridge loans are used as short-term financing solutions to cover immediate needs until more permanent funding is secured. Term loans, on the other hand, offer a lump sum of capital with a fixed repayment schedule over a set period.

The advantage of business loans is that they provide companies with the capital needed to grow, hire more employees, and expand operations. For example, a company may take out a business loan to fund a marketing campaign, purchase new inventory, or buy equipment that will increase production capacity. The key difference between personal debt and business debt is that business debt is based on the future earning potential of the company, not on past financial performance. Lenders aren’t just looking at how much money you have in the bank—they want to know if your business has the ability to generate consistent cash flow and grow over time.

However, business loans come with their own set of risks. The primary risk is the possibility of business failure. According to statistics, about 20% of businesses fail within the first year, and approximately 50% fail within five years. If your business doesn’t succeed, you could be left with a substantial amount of debt and no way to repay it. Furthermore, many business loans come with personal guarantees, meaning that if the business defaults, you are personally liable for the debt. This can put your personal assets, such as your home or savings, at risk.

For those who choose to take out business loans, the key is understanding the fine line between using debt as a growth tool and leveraging too much debt, which can put the company’s financial future in jeopardy. Proper financial planning and a clear understanding of your business’s cash flow and potential profitability are critical to making business loans work for you. Borrowing money for short-term needs can be a smart strategy, but accumulating too much debt without a clear path to profitability can lead to financial distress. When business loans are used responsibly, they can accelerate growth and open doors to new opportunities, but when mismanaged, they can quickly become a heavy financial burden.

Level 8: Leveraged Investments

Leveraged investments take borrowing to an entirely new level, shifting the focus from borrowing for consumption or business growth to borrowing for investment purposes. At this level, you’re no longer just borrowing to fund personal purchases or business operations—you’re borrowing money to amplify your returns on investments. The concept of leveraging debt for investment is based on the principle of using borrowed money to increase the potential return on an investment. While the idea may sound appealing, it introduces significant risks, as leverage can magnify both gains and losses.

At the core of leveraged investments is the idea of using debt as a tool to increase the size of your investments. For example, let’s say you have $1 million in capital, and you use it to invest in the stock market, expecting a return of 7% annually. If you borrow an additional $3 million at a relatively low interest rate (say 4%) and invest the total $4 million, your potential return increases significantly. If the investments return 10%, you could make $400,000 on your $4 million investment, compared to $100,000 if you only used your initial $1 million.

This strategy is referred to as “leverage,” and it’s common in investment markets such as real estate or the stock market. By borrowing additional money, you can invest more than you could otherwise, thereby increasing the potential returns. However, leverage also comes with substantial risk. If the market turns against you, and your investments lose value, the losses are also amplified. For instance, if your $4 million investment drops by 10%, you’re not just losing $100,000—you’re losing $400,000, and you still owe the lender their interest and principal payments.

The biggest benefit of leveraged investments is that they can significantly boost returns, allowing you to generate higher profits from your investments. For example, real estate investors often use leverage to acquire more properties than they could afford by using borrowed money to finance the purchase of additional properties. Similarly, investors in the stock market may borrow money to buy more shares, increasing their potential for higher returns.

However, leveraging investments can be risky. The key issue is that it magnifies both gains and losses, meaning that you could lose more than your initial investment if things go wrong. In addition, leveraged investments often come with higher interest rates, which can eat into your returns over time. If the investments fail to generate the expected returns, the losses can quickly escalate, and the debt can become unmanageable. The danger with leveraging investments is that you are betting not just on your own capital but on borrowed money, which increases the stakes and heightens the risk of failure.

To make leveraged investments work, you need to have a deep understanding of the market, a solid risk management strategy, and the ability to weather significant fluctuations in asset values. Using leverage for investments can be a highly effective way to increase your returns, but it’s essential to be mindful of the risks involved. Only invest borrowed money in opportunities that have the potential to deliver substantial returns, and be prepared to absorb losses if the market doesn’t move in your favor. In short, leveraged investments can serve as a powerful tool for growing wealth, but they require a high degree of caution and financial acumen.

Level 9: Corporate Debt

Corporate debt represents a shift in the scale and scope of borrowing. At this level, borrowing is no longer about personal financial decisions or even small business investments, but about fueling the growth of large companies, often with substantial revenue potential. Corporate debt is a tool used by companies to finance their operations, expand into new markets, invest in research and development, or cover day-to-day operational expenses when cash flow falls short. It can come in many forms, including bonds, loans, and lines of credit.

One of the primary reasons companies take on debt is to ensure liquidity. Even the most successful companies may experience fluctuations in their revenue streams, especially if they are involved in industries with high capital expenditures or long sales cycles. Having access to corporate debt allows these companies to maintain operations, pay employees, and cover essential expenses when cash flow is temporarily low. However, corporate debt isn’t just for weathering temporary financial storms. It’s often used as a strategic tool to fuel expansion.

For example, a company may issue bonds to raise funds for a major acquisition or to invest in new technologies that will propel the company forward. Large corporations like Apple, Tesla, and Amazon have used debt to fund their growth, expanding their product offerings, building new facilities, and entering new markets. The advantage of using corporate debt is that it allows businesses to leverage future earnings for current growth, thus accelerating their expansion. When done correctly, corporate debt can lead to exponential growth and the ability to capture larger market shares.

Corporate debt is distinct from personal debt in that it’s not based on an individual’s financial history, but rather the company’s future earnings potential. Investors and lenders assess the financial health of the company, its projected cash flows, and its ability to repay the debt. If a company is performing well, has a strong brand, and possesses a clear plan for future revenue generation, lenders may be willing to provide debt capital.

However, the risks of corporate debt are substantial. While the borrowing may allow companies to scale, it also comes with the responsibility of paying back what’s owed. If the business fails to meet its financial obligations, it could face bankruptcy, restructuring, or a loss of shareholder value. Even large corporations are not immune to these risks. Consider the collapse of Lehman Brothers in 2008, a massive financial institution that had significant amounts of corporate debt. When the company failed to meet its debt obligations, it contributed to the financial crisis that affected the global economy.

For companies taking on debt, it’s crucial to maintain a balance between using debt as a growth tool and managing the associated risks. Too much corporate debt can burden a company with high-interest payments, potentially limiting profitability and hindering growth. On the other hand, underusing debt can lead to missed opportunities for expansion and a slower pace of growth. For corporate leaders, the key is to take on enough debt to fuel growth but not so much that it jeopardizes the company’s long-term viability. This requires careful planning, robust risk management strategies, and constant monitoring of cash flow and interest payments.

Level 10: Government Debt

Government debt is the highest and most complex form of debt, involving the borrowing practices of entire nations rather than individuals or corporations. Unlike corporate debt, which is based on the potential profitability of a business, government debt is usually tied to a country’s fiscal policy and its ability to collect taxes and create money. Government debt can come in various forms, including bonds, treasury bills, and other securities issued by national governments to cover deficits in their budgets.

A government may take on debt when its spending exceeds its revenue, essentially borrowing to cover the gap between what it earns in taxes and what it spends on programs, infrastructure, defense, and other public services. When a government runs a deficit, it issues bonds that are sold to investors, other countries, or pension funds. These investors then receive interest payments on the bonds over a specified period, and the government promises to repay the principal amount at the end of the bond’s term.

Government debt serves as a vital tool for managing national economies. Countries use debt to finance infrastructure projects, social programs, defense initiatives, and disaster recovery efforts. This debt, often viewed as systemic, has become an integral part of global finance. Government debt is unique in that governments have several tools at their disposal to manage it, including the ability to print money, set interest rates, and refinance debt through new bonds.

The United States, for example, has a national debt exceeding $34 trillion, a figure that is growing annually. While this might seem like an alarming amount, governments are able to manage such massive debt loads because they can raise revenue through taxation and borrow from domestic and international investors. Unlike individuals or corporations, governments are not held to the same standards when it comes to debt repayment. A nation can issue more bonds, print money, and even renegotiate debt terms to prevent default. For these reasons, many investors consider government debt to be relatively low risk, especially when it comes to major economies like the U.S. or European Union countries.

However, while government debt is seen as safer than personal or corporate debt, it still comes with risks. As debt grows, so do the interest payments, which can crowd out funding for essential programs. The U.S. alone spends hundreds of billions of dollars annually just on interest payments for its national debt. If the economy falters, or if interest rates rise significantly, the cost of servicing debt can become unsustainable, leading to inflationary pressures, higher taxes, or cuts to public services.

In extreme cases, a country can face a sovereign debt crisis, in which it is unable to meet its debt obligations. This can lead to currency devaluation, economic instability, and, in some cases, default on national debt. A well-known example is the 2008-2009 Greek debt crisis, in which Greece faced severe economic turmoil due to its unsustainable debt levels and the inability to meet debt payments. As a result, the country had to undergo austerity measures and significant restructuring to stabilize its economy.

At the global level, government debt also has international implications. The borrowing and lending of money between countries impact global financial markets, and a country defaulting on its debt can have ripple effects that affect other economies. When the U.S. faces a debt ceiling crisis or when there’s uncertainty around government bonds, the impact is felt worldwide. International trade, currency exchange rates, and stock markets can all be influenced by shifts in government debt dynamics.

Ultimately, government debt is a complex and essential element of the global financial system. While it can be a powerful tool for managing national economies and financing long-term projects, it also carries significant risks. The ability of a government to manage debt effectively depends on its economic policies, the health of its financial system, and its ability to generate revenue. As national debts continue to rise around the world, finding a balance between borrowing for growth and managing fiscal responsibility remains one of the most critical challenges faced by modern governments.

Conclusion

The levels of debt each carry their own set of challenges and opportunities. Whether you’re struggling with payday loans or using business debt as a tool for growth, the way you manage debt will significantly impact your financial future.

Understanding the different levels of debt and the consequences of each can help you make smarter decisions, whether you’re trying to escape debt or leverage it for success. The key is to use debt as a tool rather than a trap, and always to keep your future self in mind when making borrowing decisions.