In the modern economy, the way you earn is just as important as how much you earn. Two people can report the same income on paper, yet one ends the year with a far fatter bank account—and it’s not because they worked harder. It’s because the tax system doesn’t treat all dollars equally. Wages and salaries are taxed heavily, while profits from investments and ownership are taxed far more lightly.

This disparity isn’t a hidden loophole; it’s a structural feature that shapes the fortunes of entrepreneurs, investors, and the ultra-wealthy. Understanding the difference between earned income and capital gains isn’t just a tax lesson—it’s a blueprint for keeping more of what you make, compounding it faster, and shifting from a lifetime of labor to a lifetime of ownership.

Not All Income Is Created Equal

Two people can spend a year earning the same gross figure—say $200,000—and yet their financial destinies can diverge as soon as the taxman enters the picture. For one, perhaps a corporate lawyer or a senior engineer, the government’s claim on those earnings is swift and substantial. Their paycheck is clipped before it even reaches their account, payroll taxes quietly bite off another chunk, and what remains has already lost a significant portion of its original weight.

For the other, maybe a real estate developer or long-term investor, the story plays out very differently. Their $200,000 may arrive as the result of selling shares in a company they’ve held for several years or disposing of an appreciated property. That profit is classified not as “earned” through active work, but as a capital gain—a reward for ownership, patience, and strategic timing. In tax terms, that distinction is monumental.

Earned income is tethered to your personal labor. Your time and skills are the only fuel source, and the number of hours in a week sets an immutable ceiling on how much you can produce. Worse, the tax code treats this income as the most taxable form of money—layering progressive federal rates on top of payroll taxes for Social Security and Medicare. You get taxed before you even have the chance to deploy that income into building assets.

Capital gains, however, originate from an entirely different engine. They’re born not from the sweat of your brow, but from the quiet appreciation of something you own. Whether it’s stock in a company, a parcel of land, or a piece of art, the gain reflects an increase in market value over time. And because tax authorities want to encourage such investments, they levy far lighter rates. The result is that a dollar earned through growth is worth significantly more, after tax, than a dollar earned through labor.

For those in the upper echelons of wealth, this is not an accidental bonus—it’s a deliberate choice. They design their financial lives to prioritize income streams that are taxed less, compounding the gap between themselves and those who depend solely on salaries. Over years and decades, this gap becomes not just a difference in income but a chasm in wealth.

The Three Main Types of Income

The U.S. tax code doesn’t just tax different amounts differently—it taxes different kinds of money differently. Understanding these categories isn’t just a matter of trivia; it’s the foundation of tax strategy. The three primary classifications—earned income, portfolio income, and passive income—each operate under unique rules, rates, and hidden advantages.

Earned Income

This is the most familiar and, ironically, the most heavily taxed form of income. It covers everything tied to your direct work: salaries, hourly wages, commissions, consulting fees, and self-employment pay. In 2024, federal income tax rates range from 10% for the lowest earners to 37% for the highest. For the self-employed, there’s an additional 15.3% payroll tax covering both the employer and employee share of Social Security and Medicare. Even traditional employees feel the sting—while their employer covers half the payroll tax, it still reduces the value of their labor in the broader economic equation.

What makes earned income particularly punishing is its inflexibility. It’s taxed when it’s earned, with little room to maneuver. You can’t defer it without specialized retirement accounts, you can’t offset it easily with unrelated losses, and every additional dollar you make often pushes you into a higher marginal bracket. It’s money that gets taxed before you have the opportunity to put it to work.

Portfolio Income

This category is the darling of the wealthy. It includes long-term capital gains—the profits from selling assets you’ve held for more than a year—and qualified dividends from stocks. The rates are strikingly lower: 0%, 15%, or 20% depending on your total income, with no payroll tax. This is where the gap between “working for money” and “having money work for you” becomes obvious.

The beauty of portfolio income lies in its flexibility. Gains aren’t taxed until you realize them by selling the asset, meaning you can let them grow tax-deferred for years or even decades. You can time sales to fall in lower-income years, or harvest losses to offset gains elsewhere. For those with substantial capital, this flexibility is a game of chess against the calendar—and they’re very good at winning.

Passive Income

Often overlooked by the general public, passive income covers earnings from ventures you don’t actively manage day to day—rental properties, limited partnerships, intellectual property royalties. Here, tax advantages multiply: depreciation can offset taxable income on paper, even when the property is profitable in reality; certain partnership structures allow for significant deductions; and in some cases, income can be reclassified in ways that reduce the effective tax rate.

Taken together, these three categories reveal the blueprint for how the wealthy preserve and expand their fortunes. By shifting the bulk of their earnings from heavily taxed earned income to lightly taxed portfolio and passive income, they retain more of every dollar. It’s not magic—it’s mechanics. And the tax code, whether by design or inertia, makes it clear which form of income it prefers.

The Doctor vs. The Investor

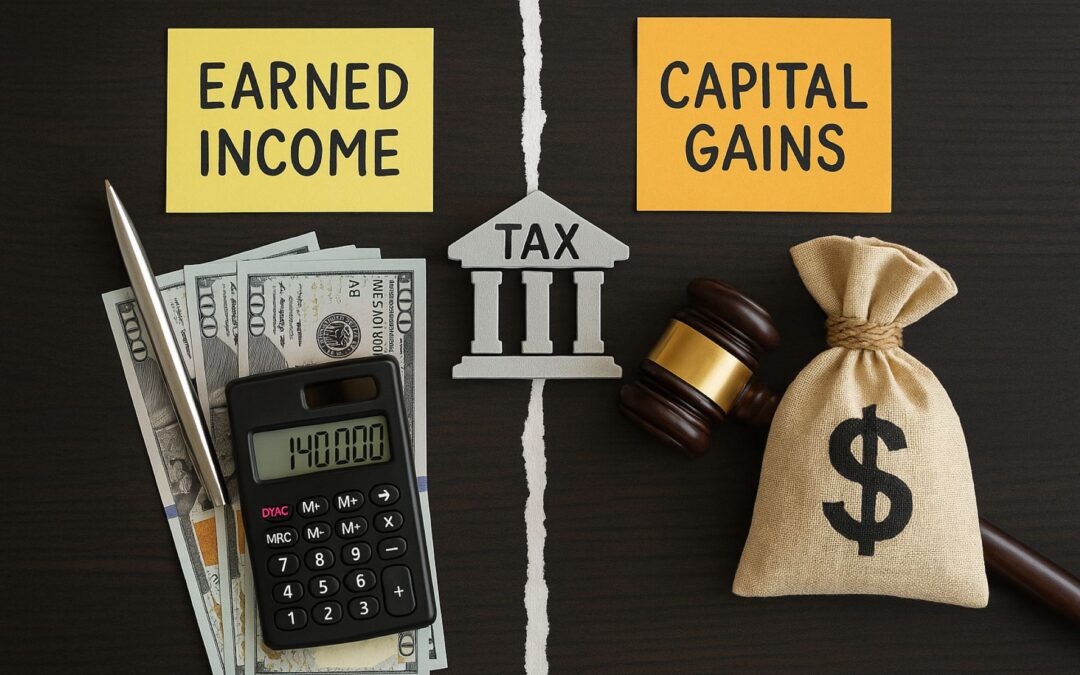

Picture two professionals, both intelligent, both driven, both ending the year with $200,000 in gross earnings. On paper, their incomes are identical. But when the dust settles after tax season, their realities could not be more different.

Person A is a high-paid professional—a surgeon, attorney, or senior executive. Their $200,000 is pure earned income. Federal tax brackets take a substantial bite: at an effective rate of 24–32%, they owe around $45,000 in income tax. If they are self-employed or run their own practice, they also shoulder the full 15.3% payroll tax for Social Security and Medicare—another $15,300. If they are an employee, that payroll burden is split with their employer, but the total cost to the system remains the same. The combined result? Roughly $60,000 siphoned away before they can invest, save, or spend it. Their take-home pay lands near $140,000.

Person B plays by a different set of rules. They’re an investor who earned their $200,000 not by logging hours, but by selling an appreciated asset—perhaps shares in a tech company they’ve held for over a year. That profit is classified as long-term capital gains, taxed at just 15% for most households in this bracket. Their tax bill is about $30,000. Payroll taxes? Zero. Their net income stands at $170,000.

That $30,000 difference is not trivial—it’s the equivalent of maxing out retirement accounts, buying a rental property deposit, or funding a year’s worth of additional investments. And because capital gains income is not tethered to hours worked, Person B can potentially repeat the process while Person A’s earnings remain constrained by time, stamina, and market demand for their skills. Over ten years, assuming equal gross incomes, Person B could be half a million dollars ahead—before even factoring in the compound growth on those extra retained dollars.

This is why the wealth gap between labor earners and capital earners expands over time: the former are taxed at the front door, while the latter stroll in through the side entrance with a smaller toll.

How the Wealthy Engineer Their Income

For the wealthy, this difference in treatment between labor and capital isn’t just an incidental benefit—it’s the core of their financial architecture. They don’t merely earn money; they design the way their money arrives, ensuring it passes through the tax system in the most favorable form possible.

1. Equity Instead of Salaries

Rather than drawing large paychecks, startup founders and corporate executives often negotiate for equity—shares in the company itself. This equity can be founder’s stock purchased at nominal cost, stock options granted as part of a compensation package, or restricted stock units (RSUs) that vest over time. By keeping their salary modest, they avoid the higher brackets and payroll taxes on labor income. The real payday arrives when they sell their equity, which is taxed as capital gains, sometimes at rates less than half of what ordinary income would incur.

2. The “Buy, Borrow, Die” Playbook

Once assets have appreciated, selling them would trigger tax. So instead, the wealthy use them as collateral to secure loans—often at low interest rates—providing spendable cash without a taxable event. These loans can finance everything from living expenses to luxury purchases, while the underlying assets continue to grow. When the owner dies, heirs receive a “step-up” in cost basis, meaning the unrealized gains vanish for tax purposes. Decades of growth are never taxed at all.

3. Leveraging QSBS (Qualified Small Business Stock)

For entrepreneurs who build and sell qualifying small businesses, the QSBS provision is a golden ticket. Hold the stock for more than five years and you can exclude up to $10 million—or ten times your investment basis, whichever is greater—from federal capital gains tax. This single exemption can turn what would have been a seven-figure tax bill into zero.

4. Timing the Realization of Gains

Because capital gains aren’t taxed until realized, the wealthy can choose when to trigger them. This timing allows them to sell in low-income years, offset gains with losses (tax-loss harvesting), or spread large sales over multiple years to remain in lower brackets.

These are not obscure tricks; they are well-established features of the tax system. But they require foresight, patience, and—most importantly—ownership of assets that grow in value. Wage earners have little flexibility: every paycheck is taxed at the source, with no chance to reclassify it. For those who prioritize ownership, however, the game shifts. Income becomes malleable, taxable only when and how they choose, and taxed less harshly when it finally appears.

Capital Gains: Income from Growth, Not Effort

Capital gains are the monetary reward for letting assets appreciate over time, rather than trading hours for dollars. When you purchase an asset—a block of shares, a parcel of land, a piece of art, even cryptocurrency—you lock in a cost basis, the original purchase price. If, over the months or years that follow, the asset’s market value rises, the difference between that cost basis and the eventual selling price is your gain.

The IRS treats these gains in two distinct ways:

- Short-term capital gains: Assets held for less than a year before being sold. These are taxed at your ordinary income rate—essentially no better than a paycheck. Sell too quickly and you forfeit the primary advantage of investing.

- Long-term capital gains: Assets held for more than a year. These enjoy far lower rates—0%, 15%, or 20%, depending on your taxable income bracket. For high earners, the top long-term rate (20%) is almost half the top earned income rate (37%).

This tax preference exists for a reason. In 1921, U.S. lawmakers deliberately structured it to encourage long-term investment in businesses and property. The rationale was simple: sustained investment fuels economic growth, job creation, and infrastructure development. The effect, however, has been to disproportionately benefit those who already have capital to invest, since they can afford to wait for long-term classification.

Another critical advantage of capital gains is the timing of taxation. You don’t owe a penny until you sell the asset and “realize” the gain. This allows investors to compound wealth for years without losing any to taxes in the meantime—a feature known as tax deferral. By contrast, earned income is taxed immediately upon receipt, reducing the amount you can reinvest right away.

When you pair lower rates with the ability to control when taxes are due, capital gains become an extraordinarily efficient vehicle for building and preserving wealth. It’s not simply that you pay less—it’s that you can keep more working for you, for longer, before the government takes its cut.

Global Tax Preferences for Capital

The U.S. is far from alone in its favorable treatment of capital gains. Across much of the developed world, governments have long recognized that investment capital is mobile and sensitive to taxation—tax it too heavily, and it may migrate elsewhere. The result is a patchwork of policies that, while differing in detail, share a common thread: they tax capital growth more gently than labor.

- United Kingdom: Capital gains are taxed at 10% for basic-rate taxpayers and 20% for higher-rate taxpayers. Compare this with the top income tax rate of 45%, and the advantage for investors is glaring. Even gains on residential property, which are taxed at slightly higher rates, still often undercut the top income brackets.

- Germany: A striking example—if you hold certain assets, such as real estate, for more than one year before selling, you can owe no capital gains tax at all. This rule effectively transforms property into a tax-free growth engine for patient owners.

- Australia: Assets held for over 12 months qualify for a 50% reduction in the taxable gain. That means an investor selling $100,000 worth of appreciation is taxed on just $50,000.

- Singapore: Takes the incentive to its extreme—there is no capital gains tax whatsoever. Investors pay nothing on profits from selling shares or property, making the city-state a magnet for global wealth.

Originally, these policies were framed as pro-growth measures. By reducing the tax burden on investment, governments hoped to stimulate entrepreneurship, expand housing markets, and encourage citizens to fund businesses. But over decades, the result has been a consistent and structural advantage for asset owners over wage earners.

In nearly every major economy, the same truth emerges: if your income comes from selling assets, you will generally keep a larger percentage of it than someone earning the same amount from wages. This preference for capital over labor doesn’t just shape personal financial strategies—it influences entire economic systems, from real estate markets to startup ecosystems, and it widens the gap between those who work for money and those who own the things that make money.

The Shift from Wages to Ownership

Over the past half-century, the relationship between labor and capital has been quietly but steadily rebalanced—and not in labor’s favor. In 1970, workers collectively took home about 64% of the nation’s income. By 2023, that share had slipped to less than 59%. In raw numbers, that decline represents trillions of dollars diverted from paychecks into profits, dividends, and other returns to capital.

At first glance, a five-percentage-point drop may seem small, but in a $27 trillion economy, it’s seismic. It means that for every dollar generated, more of it is flowing to business owners, investors, and shareholders—and less to the people whose labor helps generate it.

Part of this shift is structural. Over time, economies have become more capital-intensive, relying on technology, machinery, and intellectual property rather than large pools of human labor. Once an asset is in place, whether it’s a software platform or a factory automation system, it can generate revenue without an equivalent increase in payroll costs. Profits rise, but wages stagnate.

The divergence between asset returns and wage growth underscores this trend. Since 1990, the S&P 500—representing America’s largest companies—has appreciated more than 1,600%, not even counting dividends. Over the same period, average wages, after adjusting for inflation, have crawled up by only about 18%. This isn’t just a statistical curiosity; it’s a compounding wealth gap in motion. Those who own equities, real estate, or businesses have ridden a wave of exponential growth, while those relying solely on wages have barely outrun the rising cost of living.

And because the tax code favors capital over labor, the wealth generated through ownership is not just greater in absolute terms—it’s also more lightly taxed. This dual advantage accelerates the transfer of economic power from wage earners to capital owners, creating a feedback loop: the more assets you hold, the more income you generate, the more you can reinvest, and the further you pull ahead.

Technology and the Decline of Job Security

Technology, particularly automation and artificial intelligence, is amplifying the imbalance between labor and ownership. For much of the industrial era, productivity gains still required substantial human oversight and labor. But in the 21st century, a single software upgrade can replace entire departments. AI models can process contracts, draft marketing copy, diagnose medical images, and even generate code—tasks that once demanded specialized human expertise.

For employers, this is a dream: scalable output without proportional increases in payroll costs. For workers, it’s a growing existential threat. A 2024 global survey revealed that one in four workers fears their job will disappear within the next five years due to technological displacement. This isn’t idle paranoia; it’s already happening in industries from legal services to logistics.

Relying on earned income has always carried risks—health problems, skill obsolescence, market downturns—but technology has compressed those risks into shorter timeframes. A career that once promised stability for decades can now be disrupted in a matter of years, sometimes months. Even “safe” professional roles are increasingly vulnerable.

Assets, on the other hand, do not call in sick, require retraining, or demand healthcare benefits. A rental property doesn’t lose its ability to produce income because of a new AI model. A diversified investment portfolio can continue compounding whether you’re actively working or not. The result is a widening divide in financial security: labor income is becoming more volatile and less predictable, while capital income remains consistent and, in many cases, scalable without additional personal input.

This shift is rewriting the calculus of financial stability. In the past, job security and a reliable paycheck were considered the bedrock of middle-class life. Today, the bedrock is shifting toward ownership—toward having assets that produce income even when you’re not working. The people who understand and act on this shift are positioning themselves to weather the disruptions of the coming decades, while those who ignore it risk being permanently left behind.

The Millionaire Income Breakdown

When you examine the income sources of America’s highest earners, a striking pattern emerges: salaries make up only a sliver of their wealth. According to a 2023 IRS report, in households earning over $1 million annually, just 17% of that income came from wages or salaries. The remaining 83% was derived from capital gains, dividends, business profits, real estate income, and other investment returns.

This breakdown reveals a critical truth—the wealthy are not simply earning more at their jobs; they are earning differently. A $1 million income built primarily from capital gains and business ownership isn’t just larger in gross terms, it’s far more tax-efficient. Those capital gains might be taxed at 15% or 20%, dividends at similar rates, and business income can often be reduced through depreciation, deductions, and strategic expense allocations. The effective tax rate for such a household can easily be lower than that of a high-earning professional making a fraction of the same gross income from wages.

This structural advantage compounds over time. If a household keeps even 10–20% more of its gross income each year than an equivalent wage-earner, the difference doesn’t just add up—it snowballs. That additional retained income becomes new capital to invest, which in turn generates more lightly taxed income, further accelerating the wealth gap.

The millionaire income model is also less dependent on personal time or physical presence. A wage earner must keep producing output to maintain their income; a capital earner can step away for months without their income collapsing. The income streams of the wealthy are designed to survive vacations, illnesses, even retirements, because they’re rooted in ownership, not labor. This resilience is one reason why, during economic downturns, wealthy households can often continue building wealth while wage-dependent households struggle just to hold their ground.

The Future Belongs to Owners

Jobs remain essential, especially for building initial capital, gaining experience, and establishing credibility. But the economic landscape is shifting toward a clear reality: long-term freedom is not built on working more hours—it’s built on owning more productive assets.

Ownership changes the entire dynamic of wealth creation. When you own a rental property, a portfolio of dividend-paying stocks, or a business with a management team in place, your income is no longer limited by the hours you can work. Assets can operate continuously, generate revenue while you sleep, and scale without demanding more of your time. This is the essence of financial leverage—not borrowing more, but achieving more output from the same input of personal effort.

The tax code reinforces this shift. In the U.S. and many other countries, investment income enjoys preferential tax rates, exemptions, and deferral opportunities. Ownership allows you to control the timing of taxable events, offset gains with losses, and reinvest pre-tax growth. Wage earners have none of these luxuries—every paycheck is taxed on arrival, reducing the amount that can be deployed toward wealth-building.

In the coming decades, the gap between owners and non-owners is likely to widen. Automation, AI, and global competition will continue to pressure wages, while capital will remain scalable and mobile. The people who adapt early—by turning earned income into assets that produce portfolio and passive income—will position themselves for lasting financial independence.

This doesn’t require starting with millions. Even modest ownership, begun early and expanded consistently, can transform financial outcomes over a lifetime. The key is to treat wages as a temporary phase, a tool for acquiring the real engine of wealth: assets that generate income without your daily presence. In a world where the future belongs to owners, those who cling solely to labor will be working harder for less, while those who own will enjoy both time and financial freedom.

Conclusion

The tax code quietly reveals a truth the wealthy have acted on for generations: it’s not enough to earn more—you must earn differently. Wages provide a start, but ownership provides freedom. Capital gains, dividends, and passive income streams aren’t just taxed more favorably; they’re also untethered from the limitations of time and personal effort. The future of financial security belongs to those who convert labor income into income-generating assets, letting money work harder than they ever could.

Whether your first step is buying shares, starting a side business, or acquiring a rental property, the principle remains the same—own more, work less, and structure your income so that you keep more of every dollar. In a world where the rules reward ownership, the sooner you play that game, the sooner you stop running on the treadmill and start building a legacy.