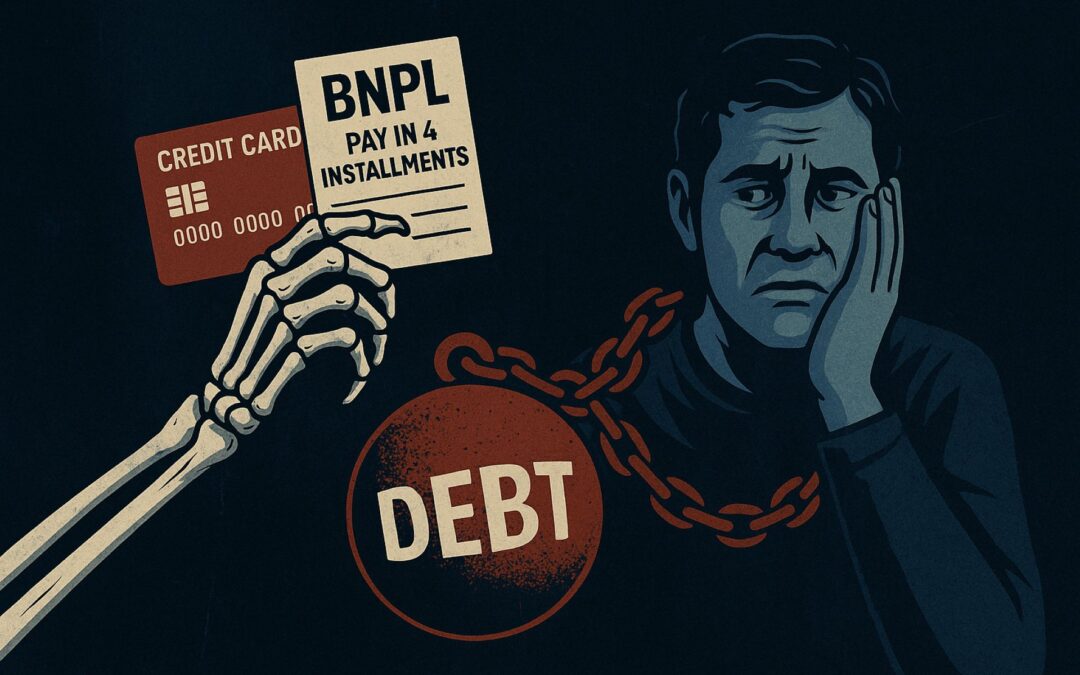

As of 2025, nearly half of consumers—49%—use buy now, pay later (BNPL) services like Clara, Afterpay, and Affirm. Meanwhile, the average American carries over $10,000 in debt, with total U.S. credit card balances skyrocketing to an eye-watering $1.18 trillion. That’s trillion—with a capital T. But this isn’t a coincidence. It’s the outcome of deliberate psychological engineering designed to keep people spending and indebted.

The Debt Machine: Credit Cards vs. Buy Now Pay Later

At face value, traditional credit cards and buy now, pay later (BNPL) services seem to serve different purposes, catering to different types of consumers and shopping experiences. Credit cards have been ingrained into the fabric of financial life for decades. Most people carry them in their wallets, swipe or tap them daily without a second thought, and regard them as an essential convenience. They offer revolving credit, allowing users to make purchases up to a set limit and pay back the borrowed amount over time, usually with interest if the balance isn’t paid off promptly.

Buy now, pay later services, on the other hand, are a relatively new phenomenon that exploded alongside the rise of e-commerce. These apps—like Clara, Afterpay, and Affirm—promise to break down the total cost of a purchase into smaller, more manageable installments, often interest-free, making it feel more affordable. You’ll see their logos flashing at online checkouts, tempting consumers with the option to “pay in four easy installments,” transforming a single, sometimes intimidating payment into a series of smaller ones. This approach feels modern, frictionless, and appealing to those wary of traditional credit cards.

Yet, beneath these surface differences, the two systems operate on the same foundational principle: they give you access to money upfront, but you pay for it later. They create a bridge between desire and affordability, essentially advancing you funds you don’t yet have.

But how exactly do these companies profit from this arrangement?

Every time you use a credit card or BNPL option to pay, the company processing the transaction charges a fee—this fee comes out of the merchant’s revenue. For credit card companies like Mastercard or American Express, the cut usually ranges from 2% to 3% of the transaction value. BNPL providers, however, charge even more—typically between 4% and 6%. On a $100 purchase, this means the credit card company might claim $2 to $3, whereas a BNPL platform could pocket $4 to $6.

Why would any business willingly give up such a chunk of its sales?

The answer lies in consumer psychology and conversion optimization. When shoppers hesitate at checkout—especially faced with a large total—they are prone to abandon their carts. BNPL services solve this by fragmenting the payment into smaller chunks, reducing the immediate financial burden and lowering the perceived barrier to purchase. Suddenly, that intimidating $100 feels like four manageable $25 payments, and the consumer is more likely to complete the purchase.

From the retailer’s perspective, this increase in completed sales and higher average order values compensates for the processing fees. They accept paying a higher cut to BNPL companies because it often means more revenue overall. Meanwhile, the BNPL services thrive on volume, growing their profits as more consumers opt into these installment plans.

Traditional credit cards similarly benefit from increased spending prompted by deferred payment and rewards programs, though they face more regulatory scrutiny and longer-established consumer protections.

In essence, both credit card companies and BNPL providers have become finely tuned debt machines, leveraging behavioral economics to maximize spending. They design their systems not just to facilitate payment, but to subtly coax consumers into borrowing more, spending beyond their means, and locking into long-term repayment obligations—often without fully appreciating the true cost until it’s too late.

Spending More, Impulsively and Unaware

The subtle yet powerful design of credit cards and buy now, pay later (BNPL) services does more than just facilitate purchases—it actively encourages consumers to spend more than they originally intended. This phenomenon isn’t just anecdotal; a wealth of research underscores that people tend to spend more per transaction and exhibit more impulsive buying behavior when using these payment methods compared to cash.

Why does this happen? The answer lies in the psychological distance created between the act of spending and the actual outflow of money. When paying with cash, the transaction is tangible: you physically hand over bills and coins, and you witness your wallet thinning. This creates a mental “pain of paying” that instinctively triggers caution and more deliberate decision-making. The immediate loss is salient and real.

In contrast, swiping a credit card or tapping a phone feels almost intangible. The money leaves your account electronically, often without any immediate physical sensation. You don’t see the money physically leave your hands. This creates what psychologists call “payment decoupling” — the separation between the pleasure of acquiring something and the discomfort of spending money. The mental friction that usually curbs excessive spending evaporates.

BNPL services amplify this effect even further by spreading the cost across several smaller payments. The psychological impact of seeing a $100 price tag is replaced by a series of smaller numbers, such as four payments of $25, which seem more manageable and less threatening. This fragmentation of cost blunts the perceived expense, allowing consumers to justify purchases they might otherwise hesitate over or abandon altogether.

Moreover, retailers are acutely aware of this behavioral tendency. They strategically position BNPL options prominently during checkout, often with enticing language like “interest-free installments” or “pay later,” encouraging consumers to opt in. This design taps directly into our cognitive biases, reducing resistance and enhancing conversion rates.

Studies have demonstrated that not only do consumers spend more per transaction when using these methods, but they also tend to buy more frequently and tip more generously in service contexts. The decrease in perceived spending pain causes consumers to loosen their financial reins overall, leading to an increase in overall expenditure.

This dynamic creates a feedback loop beneficial to merchants and payment providers but detrimental to the consumer’s financial health. The retailer gains higher sales volumes, the BNPL or credit card company collects larger processing fees and potential interest, but the consumer often ends up saddled with unexpected debt.

What’s particularly insidious is how this impulsive spending often happens without consumers’ conscious awareness. They believe they are exercising control and making savvy financial decisions, but in reality, the frictionless nature of these payment systems hijacks their decision-making processes.

Ultimately, this elevated and impulsive spending behavior is a crucial part of why credit card debt and BNPL usage have ballooned in recent years. The seamless convenience and clever psychological framing encourage consumers to spend more freely today while pushing the burden to an abstract, future date—often with costly consequences lurking just beyond the horizon.

The Hidden Cost of Missing Payments

While buy now, pay later (BNPL) services and credit cards often advertise enticing offers—0% interest, no fees, and flexible payment schedules—there’s a dark underbelly lurking beneath these seemingly benign promises. The true cost emerges most starkly when payments are missed or delayed, triggering a cascade of financial penalties that can quickly spiral out of control.

For credit cards, the marketing narrative emphasizes grace periods and promotional rates, but these benefits hinge entirely on punctual payments. Miss a due date, and the consequences can be severe: late fees, penalty interest rates that sometimes exceed 23% annually, and compounding interest charges that exponentially increase what you owe. What starts as a small slip can snowball into an overwhelming debt mountain.

BNPL services operate similarly, but their structure can be even more deceptive. The initial appeal is the simplicity of splitting a purchase into equal, interest-free installments. However, if a payment is missed, fees and interest charges kick in—sometimes at surprising rates—and the consumer’s credit score may take a hit. Unlike traditional loans, BNPL platforms often have less transparent terms, making it harder for users to fully grasp the potential fallout of missing a payment.

Moreover, the business model of these companies often revolves around profiting not just from timely payments but disproportionately from those who fall behind. The least reliable and most forgetful customers become the biggest revenue drivers, as fees, penalties, and interest accumulate rapidly. This creates a predatory dynamic, where financial vulnerability is exploited to maximize profits.

An important nuance lies in how these companies treat different segments of customers. High-net-worth individuals—those charging $10,000 dinners or luxury goods on American Express cards—often enjoy low or zero interest rates indefinitely. They receive perks, VIP service, and leniency because their spending volume guarantees significant fees for the card issuers.

Conversely, everyday consumers, especially those relying on BNPL for groceries, fast food, or small purchases, face harsher treatment. Missing a single payment can trigger a slew of fees and financial consequences, disproportionately penalizing those with fewer resources and less financial flexibility.

This tiered approach mirrors casino practices: high rollers receive complimentary upgrades and free drinks, while the average player is systematically charged for every mistake or delay. The analogy extends further—the system is designed to keep the wealthy “winning” while extracting money relentlessly from those struggling to keep up.

The consequences for the consumer are grave. Many don’t realize they are trapped in this cycle until it’s too late, blindsided by growing balances and mounting fees. The initial convenience of deferred payment morphs into a burdensome trap, where debt becomes unmanageable and creditworthiness deteriorates.

Ultimately, this hidden cost structure is a crucial element in the explosion of consumer debt. It thrives on behavioral lapses, forgetfulness, and the human tendency to underestimate future financial strain. The system preys on these vulnerabilities, turning missed payments into profit engines and deepening economic inequality.

Understanding this reality is vital for consumers seeking to navigate the modern financial landscape. The “interest-free” veneer is fragile, and the penalties for missteps are real and punishing. Vigilance, intentional budgeting, and skepticism toward seemingly generous credit offers are essential defenses against falling victim to this insidious aspect of debt.

Psychological Traps Behind the Spending Frenzy

Understanding why consumers so readily fall into this debt cycle requires examining the sophisticated psychological manipulation baked into BNPL and credit card systems. These companies exploit innate human biases and neurological responses, creating traps that subtly erode financial discipline.

Frictionless Spending: The Painkiller Effect

One of the most powerful psychological levers that credit card companies and buy now, pay later (BNPL) services exploit is the concept of friction—or rather, the absence of it—in spending. Paying with cash is a sensory and deliberate act. You physically count out bills or coins, feel the weight of the money leaving your hand, and watch it change hands. This creates a tangible sense of loss, a psychological “sting” that triggers caution and slows down impulsive behavior.

Contrast this with the ease of swiping a card or tapping your phone. The transaction happens in a split second, often without any visible exchange or immediate consequence. This near-instantaneous process removes the physical and emotional “pain” of parting with money. When payment is effortless, your brain registers less resistance to spending.

Psychologists call this phenomenon the “pain of paying,” and it is a crucial behavioral checkpoint. Cash enforces it; cards and digital payments bypass it.

Studies consistently show that consumers spend significantly more when using credit cards versus cash. One explanation is that friction acts as a brake on spending, forcing you to consciously consider each purchase. Without it, that mental pause disappears.

BNPL services heighten this effect by fragmenting payments into smaller, painless chunks. Rather than confronting a single, often intimidating sum, consumers are presented with bite-sized installments that feel manageable and less threatening. The cost is psychologically diluted, even though the total remains the same or more.

This frictionless spending acts like a painkiller, dulling your financial awareness and making it easier to overspend without fully processing the consequences. It’s a form of behavioral numbing engineered to accelerate purchasing decisions.

Ultimately, when spending feels painless and instantaneous, consumers tend to spend more frequently and buy items they might otherwise hesitate over, fueling a cycle of impulsive consumption and mounting debt.

Dopamine Activation: The Buyer’s High

Another deeply ingrained psychological trap is the dopamine surge triggered by the act of purchasing itself. Dopamine, a neurotransmitter often associated with pleasure, reward, and motivation, plays a central role in how we experience satisfaction and form habits.

Interestingly, the dopamine hit doesn’t come primarily from using or even receiving a product—it arrives at the moment of purchase. When you swipe your card or complete a BNPL checkout, your brain rewards this action with a jolt of dopamine, giving you a fleeting sense of accomplishment and gratification.

This neurological reward system evolved to reinforce behaviors that improve survival, but in the context of modern consumerism, it’s hijacked to promote spending.

The instant gratification felt during the purchase encourages repetition. It’s the same brain pathway activated by addictive behaviors such as social media scrolling, sugary treats, and gambling. This creates a feedback loop: every purchase triggers a dopamine reward, which conditions you to seek out that pleasurable sensation again.

Buy now, pay later services design their user experience to maximize this dopamine activation. Quick checkout flows, instant approval, and visually rewarding interfaces amplify the feeling of immediate reward, making the process addictive. They tap into your brain’s craving for quick hits of pleasure, steering you toward spending more frequently and impulsively.

Over time, this dopamine-driven cycle can lead to compulsive buying, where the urge to experience the “buyer’s high” outweighs rational financial decision-making. You aren’t just buying a product; you’re chasing the rush that comes with the purchase.

This engineered gratification makes it harder to resist temptation, blurring the lines between want and need, and embedding spending habits that chip away at your financial stability without your conscious awareness.

Present Bias: The Lizard Brain’s Preference for Now

At the core of many financial pitfalls lies a primal instinct known as present bias—the tendency for humans to prioritize immediate rewards over future benefits, even when delaying gratification would be more advantageous. This cognitive shortcut dates back to our evolutionary past, when securing resources quickly was essential for survival. Our brains are wired to conserve energy and favor options that deliver instant payoffs.

Buy now, pay later (BNPL) services expertly capitalize on this ancient wiring. The very phrase “buy now, pay later” zeroes in on the most enticing part: immediate acquisition with deferred cost. Your brain locks onto the “buy now” segment, attracted by the promise of instant gratification, while the “pay later” part becomes background noise—abstract, distant, and easy to ignore.

This exploitation of present bias effectively short-circuits rational decision-making. The pain and responsibility of payment are shifted to a nebulous future, making the purchase feel almost costless today. Even if there’s an impending financial consequence, the brain’s focus on the immediate reward overwhelms the cognitive ability to anticipate and evaluate future risks.

Marketers and product designers engineer the user experience to minimize reminders of deferred payment. BNPL platforms present offers with minimal friction—no credit checks, no lengthy disclosures—so the consumer’s attention stays fixated on the immediate benefit. Notifications about upcoming payments are often subtle or delayed, ensuring the “pay later” part stays out of sight and out of mind.

This psychological trap fosters a disconnect between spending and budgeting, making it easy for consumers to accumulate multiple small debts they feel detached from. It’s a textbook example of how our “lizard brain” hijacks financial decision-making, driving behavior that, while gratifying in the moment, leads to long-term consequences that are harder to confront.

Underestimation Bias: Future You as a Financial Superhero

Closely intertwined with present bias is underestimation bias—the cognitive error where individuals overestimate their future financial capacity, willpower, or time to resolve debts. It’s that little voice inside your head whispering, “I’ll be able to afford this next month,” or “Future me will handle it,” despite current evidence to the contrary.

This form of optimism is deeply ingrained but often misplaced. It’s rooted in a mental projection that future circumstances will magically align to cover present overextensions. Consumers convince themselves that an incoming paycheck, a bonus, or lifestyle changes will solve any financial tight spots created by using credit cards or BNPL plans.

Credit card companies design their products around this optimism. They provide users with credit limits—sometimes quite generous—relying on the fact that most will believe they can manage repayments later, even as balances inch upward. The revolving nature of credit allows consumers to push their borrowing boundaries continually, feeding into this false sense of temporary overreach.

BNPL services exacerbate this bias by framing repayments as easily manageable installments, reinforcing the illusion that future payments will be painless. Consumers often fail to account for overlapping debts or unexpected expenses that could derail this optimistic timeline.

Unfortunately, reality often diverges sharply from these expectations. Unexpected bills, job changes, or simple forgetfulness collide with optimistic assumptions, leading to missed payments, fees, and spiraling debt.

Underestimation bias clouds judgment, undermines budgeting discipline, and fosters a dangerous cycle of borrowing predicated on an idealized future self that rarely materializes. Recognizing and countering this bias is essential to avoid the pitfalls of overextension and financial denial.

Financial Denial: Debt Disguised as a Feature

One of the most insidious psychological traps engineered by buy now, pay later (BNPL) services is financial denial—a cognitive blind spot where borrowing is camouflaged as a convenient payment option rather than what it truly is: debt. Unlike traditional loans or credit cards, which require applications, credit checks, and formal agreements, BNPL platforms embed borrowing seamlessly into the shopping experience, erasing the moment of pause where a consumer might reconsider taking on debt.

Imagine browsing an online store, adding items to your cart, and at checkout, you’re offered the choice to “split your payment into four easy installments.” There’s no loan officer, no lengthy contract, no explicit warning that you’re committing to repay borrowed money. This ease and invisibility make BNPL feel like a feature—a helpful budgeting tool—rather than a financial obligation.

This lack of transparency fosters denial on multiple levels. Many users simply forget or refuse to acknowledge that they owe money. The payments feel detached from the traditional concept of debt because there’s no immediate lump sum, no bills arriving in the mail, and no upfront interest. Instead, the borrowing is fragmented and disguised as “interest-free” or “fee-free” until it isn’t.

This cloak of convenience can lull consumers into a false sense of security, eroding financial awareness. Without clear reminders of their outstanding obligations, users may accumulate multiple BNPL plans simultaneously, underestimating the total amount owed.

The danger of financial denial is profound: it delays recognition of financial strain until it becomes acute. By the time missed payments and fees surface, many find themselves overwhelmed, with limited options to recover.

Ultimately, BNPL’s design to mask borrowing as a helpful payment feature is a deliberate tactic that exploits cognitive biases and lowers consumers’ defenses. It’s a psychological sleight of hand that makes debt invisible until it’s dangerously real.

Algorithmic Matching: Personalized Temptation

Behind the smooth surface of BNPL and credit card offerings lies a sophisticated web of data-driven psychology: algorithmic matching. These companies don’t simply offer generic payment options; they tailor offers to individual consumers based on extensive tracking of habits, preferences, and behavioral responses.

Algorithmic matching uses real-time data and machine learning models to identify which payment structures, phrasing, or timing will most effectively nudge a specific consumer toward spending. For example, if past behavior shows you respond favorably to “4 easy payments,” the system will prioritize presenting that option. If another user reacts better to “split into monthly installments,” the algorithm adapts accordingly.

This personalization extends to timing as well. BNPL platforms may delay showing payment reminders or offers until moments when a consumer is most receptive—such as browsing certain categories or during peak purchasing hours.

The goal is to trigger the psychological buttons that make saying “yes” to borrowing feel effortless and even desirable. Whether it’s creating a sense of safety, appealing to your sense of savvy financial management, or making you feel like you’re “getting away with something,” these algorithms fine-tune the user experience to maximize conversion.

What makes algorithmic matching particularly powerful—and dangerous—is its invisibility. Users believe their choices are autonomous and self-directed, unaware of the tailored nudges guiding their behavior. This subtle manipulation reinforces spending patterns, making consumers more likely to accept BNPL options repeatedly and with increasing frequency.

In essence, algorithmic matching turns financial decision-making into a personalized marketing game, designed to exploit your unique psychological vulnerabilities. It’s a cutting-edge strategy that blurs the line between persuasion and manipulation, all in service of driving consumer debt.

Gamification: Spending as a Level-Up

Gamification is a psychological strategy that transforms mundane or challenging tasks into engaging experiences by incorporating game-like elements—points, levels, rewards, and achievements. In the world of finance, credit card companies and buy now, pay later (BNPL) platforms have embraced gamification to make spending and repayment feel like a rewarding progression rather than a burdensome obligation.

Take American Express, for example. Rather than simply issuing a card, they create an aspirational journey through tiers—green, gold, platinum, and black cards. Each tier symbolizes a higher “level” with exclusive perks, enhanced status, and elite benefits. Users feel as if they’re unlocking achievements, which taps into the same motivational circuits in the brain that drive video game play. The desire to “level up” encourages cardholders to spend more and manage payments promptly to maintain or advance their status.

BNPL apps use similar tactics. When users successfully repay purchases on time, they are often rewarded with increased spending limits or access to premium features. This creates the illusion of earning trust or “unlocking” financial privileges. The sense of progression fosters loyalty and motivates ongoing engagement with the service.

This gamified experience obscures the reality that spending more or borrowing larger sums isn’t necessarily positive—it’s behavioral conditioning designed to encourage deeper financial entanglement. The brain interprets these milestones as victories, but in truth, they are just indicators of growing indebtedness.

By framing financial behavior as a game with rewards and levels, these companies exploit innate human desires for achievement and recognition. This leads consumers to associate borrowing and spending with positive feelings, making it harder to resist increasing debt levels. The gamification of finance cleverly disguises risk behind the allure of progress and accomplishment.

Cognitive Overload: Juggling Mini Loans

Cognitive overload occurs when the demands on an individual’s mental processing capacity exceed their ability to cope, leading to mistakes, avoidance, or paralysis. Buy now, pay later (BNPL) platforms exploit this by fragmenting purchases into multiple, overlapping installment plans—each effectively a separate mini loan with its own payment schedule, amount, and due date.

Imagine making five separate purchases using BNPL. Instead of managing one debt with a single payment timeline, you’re juggling five distinct repayment plans simultaneously. Each requires attention to detail: tracking due dates, amounts owed, and managing payments individually. This multiplication of financial commitments overwhelms working memory and executive function, increasing the likelihood of missed payments and errors.

The cognitive burden is compounded by the lack of unified billing or automated reminders. Users must manually monitor and pay each installment, creating a chaotic mental ledger that’s difficult to maintain over time. The more purchases made, the heavier the cognitive load becomes, pushing consumers toward avoidance behaviors—ignoring payments or delaying action altogether.

This isn’t a flaw or oversight; it’s a deliberate design feature. The fragmentation of debt into multiple mini loans creates confusion and mental fatigue, which BNPL companies capitalize on. Overwhelmed consumers often succumb to procrastination or denial, triggering late fees, penalties, and increased interest—additional revenue streams for the lenders.

Cognitive overload thus becomes a powerful trap, turning what might have been manageable debt into a tangled web of obligations that strain mental resources and financial well-being. Recognizing this effect is crucial for consumers aiming to maintain control over their finances and avoid falling into spirals of missed payments and escalating fees.

Conclusion

This unraveling of the dark psychological tactics behind credit cards and buy now, pay later apps reveals an uncomfortable truth: these systems are engineered to profit from your impulses, oversights, and innate human biases. The only way out is to cultivate mindfulness around spending, resist frictionless temptation, and demand financial clarity.

Your financial freedom depends not just on your income, but on your ability to see through the smoke and mirrors and take control of your relationship with money.